Issue #7 - April 2026 North Star Briefing sails where headlines meet consequences. This issue charts the…

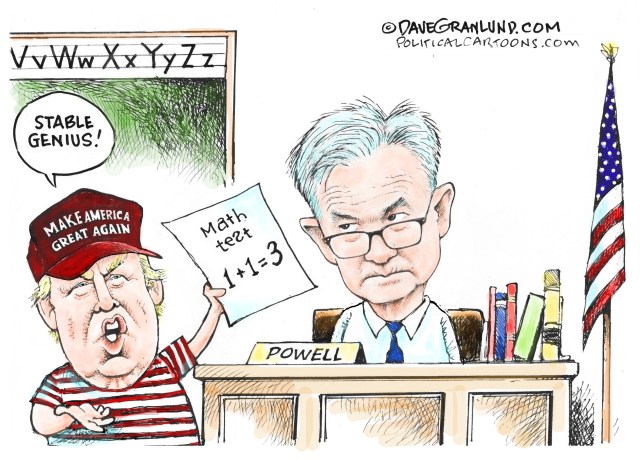

Mortgage Rates Reality Check | North Star Briefing (Nov 2025)

ISSUE # 2 – November 2025

Editor’s Note

This month: Mortgage Rates Reality Check-Interest rates sneak into your mortgage, media spin muddies the facts, and Europe dusts off its war boots. Plus: Can housing still make you rich? Your turkey come with a Michelin star? And why gratitude might be your secret weapon.

Need a steady hand?

I help bankable-but-not-bank-shaped clients identify and fix the root problem—then fund the right solution.

-

Rate Radar – Why Mortgage Rates Don’t Obey the Fed

-

Harbor Report – Why Residential Real Estate Still Wins

-

Stateside Signals – White House Renovations & Deportations

-

Open Seas Outlook – Europe’s New Air: No-Fly Zones

-

Galley & Grit – How Not to Ruin the Turkey This Thanksgiving

-

Moral Compass – Gratitude, On Purpose

-

Beacon in the Storm – Dysfunction in the Government

Ready to move? Free coaching consult or capital options—your call.

858-229-7199 – jdevilliers@c2financial.com

Rate Radar

Need clarity?

I help find the strategy that earns its financing: address the problem, then fund what works.

Harbor Report

Why Residential Real Estate Still Wins (Yes, Even If You Bought at the Worst Time)

Let’s kick off with a quote that’s been passed around more times than a holiday fruitcake:

“Ninety percent of all millionaires become so through owning real estate.”

Was it Andrew Carnegie who said that? Maybe. Maybe not. But let’s not fact-check our way out of a good north star. Because when it comes to building wealth, few things beat owning a place other people pay you to live in.

What if You Bought at the Top?

Imagine this: It’s 2006. You just bought a house at what turned out to be the absolute Everest of the real estate market. Then, like a bad hangover, prices dropped 30% over the next six years. Brutal, right?

But here’s the twist: if you didn’t panic-sell, that 30% haircut eventually grew back. In fact, by 2024, national home prices had blown past those old highs. And while prices were playing rollercoaster, rents were doing something far less dramatic: marching steadily upward. Vacancy rates? Dropping. Supply tightened. Demand didn’t.

So yes, the brave (or stubborn) who held on ended up just fine. More than fine, actually—they won.

The Secret Sauce: Leverage (a.k.a. Borrowing Like a Genius)

Now let’s talk about the unsung hero of real estate: leverage. Most people treat it like a dull footnote. But in real estate, it’s the main event.

Enter the DSCR loan—Debt-Service Coverage Ratio. Sounds like a sleep aid, but it’s actually a brilliant financing trick. Instead of qualifying based on your W-2 income, these loans are based on the property’s own cash flow (rent ÷ PITIA). It’s like your rental is getting the mortgage for you.

With 15–20% down, you can control a $500,000 asset using $75–100K of your own money. Try convincing a brokerage to lend you 80% on a 30-year note to buy stocks. They’ll laugh you right off the platform.

Here’s what that kind of leverage means over time:

-

Appreciation works overtime: A mere 3% annual bump on a $500K property = $15K. That’s a 15% return on your $100K down. And we haven’t even touched cash flow or principal paydown.

-

Fixed debt, rising rents: Inflation gets a bad rap, but for landlords with fixed loans, it’s your invisible employee. Rents rise. Your payment doesn’t. Margin = fatter.

-

Debt gets lighter: Each year, your loan stays the same while the dollar gets weaker. It’s like paying off your mortgage with Monopoly money.

-

Forced savings: Every mortgage payment chips away at principal. Unlike stocks, this builds equity whether or not the market’s in a good mood.

The “Don’t Be Dumb” Disclaimer

Now, let’s not romanticize leverage. It cuts both ways. Used poorly, it’s how people end up on late-night foreclosure infomercials.

So: do the math. Account for real taxes, insurance, maintenance, and management. Stress-test the deal—assume interest rates go up 1–2%, or rents take a temporary dip. If it still cash flows under pressure, you’ve got a margin of safety. Congratulations, you’re an adult investor.

The 2006 Case Study, Revisited

Even if you bought at the peak, you could’ve come out ahead—if you:

-

Bought cash flow, not a flip fantasy.

-

Kept tenants happy and units occupied.

-

Let rents rise with the tide.

-

Let time do its slow, boring compounding thing.

What would you have today? Higher rents. Recovered (and then some) property value. A fixed loan that’s now cheap in real dollars. And equity built from both appreciation and mortgage paydown.

It’s not flashy. But wealth creation rarely is.

So… Where Does DSCR Fit Now?

DSCR isn’t a cheat code. It’s a filter. It forces you to focus on the one thing that matters most: income. If a deal works at today’s interest rate and survives a little financial turbulence, then what you’ve got is an asset with upward-adjusting revenue and fixed costs.

Rates improve? Refinance. Rates don’t? You’re still collecting rent.

Bottom Line

Residential real estate remains one of the few places where ordinary people can buy a long-term asset with cheap, predictable leverage—backed by a product everyone needs: shelter.

-

Prices recover.

-

Rents reset.

-

Time rewards patience.

Buy for income. Stress-test the numbers. Then let tenants, time, and amortization quietly build your wealth while you do more glamorous things—like arguing about interest rates online.

Ready to move? Walk out of our first consultation with a 3-step plan that makes financing optional, realistic—and powerful when used.

With access to C2 Financials’ 100+ lenders and decades of personal experience in building, turning around and managing companies, raising capital, and running M&A I can help provide solutions to maximize your operations and secure optimal funding.

858-229-7199 – jdevilliers@c2financial.com

Stateside Signals

White House Renovations, Deportation Derangement, and Other Media Mirage Magic

“News is what somebody, somewhere, wants suppressed; all the rest is advertising.”

— Lord Northcliffe (Alfred Harmsworth), who clearly time-traveled to 2025, glanced at CNN, and promptly fainted.

Though he said it in the early 1900s, Lord Northcliffe might as well be the keynote speaker at today’s media circus. Nowhere is this more obvious than in how the press treats U.S. presidents — particularly one orange-hued former reality TV host who lives rent-free in America’s collective amygdala: Donald J. Trump.

To say the press despises him is like saying cats “tolerate” water. With the intensity of a Shakespearean blood feud, every decision made under Trump gets dissected, demonized, and declared a harbinger of doom — even when it’s something as exciting as… new carpet.

Case #1: White House Renovationgate™

Historically, presidents have tinkered with the White House like bored millionaires on a Home Depot spree. Let’s review:

- George W. Bush (2006–07): Ripped out the Situation Room and replaced it with something out of 24.

- Barack Obama (2010–14): Spent $376 million upgrading the infrastructure, possibly including a secret Batcave and a regulation basketball court.

- Donald Trump (2017): Replaced some carpets and slapped on fresh paint. Total cost: $1.75 million. Cue the media’s spontaneous combustion.

- Joe Biden (2023): $50 million to upgrade the Situation Room. Mahogany everywhere. Somewhere, Ron Burgundy smiled.

- Donald Trump Again (2025): Demolished the East Wing to build a ballroom. Chaos ensued. Headlines ranged from “Democracy Dies in Demolition” to “Dictator Declares Dance Floor.”

Note: When Obama added luxury; it was progress. When Trump adds drapes; it’s fascism. Welcome to Advertising 101.

Case #2: Deportations and Selective Memory Syndrome

Let’s now visit the enchanted realm of immigration policy, where numbers are real but reporting is optional.

Deportation Totals (Formal Removals Only):

| President | Total Removals |

| George H. W. Bush | 141,326 |

| Bill Clinton | 863,958 |

| George W. Bush | 2,021,965 |

| Barack Obama | 2,749,706 ← Winner! |

| Donald Trump (1st Term) | 935,346 |

| Joe Biden | 545,252 |

| Trump (2nd Term, partial) | 400,000 |

If deportation were an Olympic sport, Obama would’ve taken gold while Trump tripped over his shoelaces. But did you hear about this on the news? Of course not. That would’ve ruined the whole “Trump = Cruel Tyrant Who Eats Kittens” narrative.

Case #3: Who Let the Illegals In?

Let’s talk encounters — the bureaucratic term for when U.S. agents go “Excuse me, sir, do you have any fruit or terrorist connections to declare?” at the border.

Border “Encounters” by President (Rounded Trends):

- Clinton (’90s): 1M+ per year. A golden age of sneaky crossings.

- George W. Bush: Declining as the economy tanked. Border agents got lonely.

- Obama: Down to 300k–500k/year. Must’ve installed invisible fences.

- Trump (1st Term): Spiked in 2019 (~860k), then dropped. Blamed for both.

- Biden: Record highs.

- 2021: 1.66M

- 2022: 2.38M

- 2023: 2.47M ← And the crowd goes wild!

- 2024: 1.53M (People got tired of walking?)

- Trump (2nd Term, FY2025): ~240k and falling. Fewer crossings, but also fewer headlines. Apparently, low numbers don’t make good clickbait.

Conclusion: All the News That’s Fit to Omit

Imagine if the press actually reported news instead of dressing ideology in the drag of journalism. If they pointed out that deportations were highest under Obama. That Biden oversaw the largest number of illegal border encounters in history. That Trump’s East Wing renovation wasn’t exactly Versailles 2.0.

But truth doesn’t drive ratings. Outrage does. And until that changes, journalism will remain a performance art — and not the good kind with berets and espresso.

So yes, Lord Northcliffe was right: the real news gets suppressed. The rest is just advertising — and bad advertising at that.

Need a steady hand?

I help bankable-but-not-bank-shaped clients identify and fix the root problem—then fund the right solution.

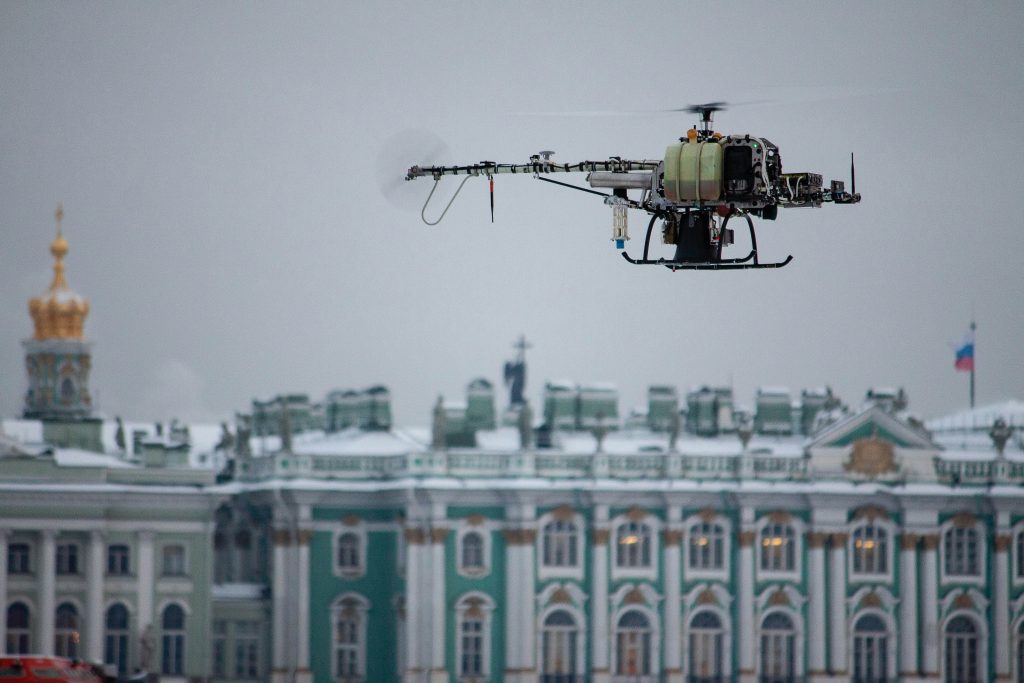

Open Seas Outlook

Photo by Andrey Kremkov on Unsplash

Photo by Andrey Kremkov on Unsplash

Europe’s New Air: From No-Fly Zones to Flying Lawn Mowers

Europe has finally accepted a harsh new reality: air superiority no longer comes from swaggering fighter jets and Top Gun remakes—it comes from cheap flying toasters with GoPro cameras duct-taped to them.

Welcome to the era of drone warfare, where NATO now talks about building a “drone wall”—a phrase that sounds like something your uncle invented after watching too many sci-fi reruns. Brussels, in its classic “measured haste,” is funding flagship counter-drone projects and shoring up its eastern flank with sensors, jammers, and enough mesh networks to make a cyberpunk novelist weep.

Translation: fewer parades, more PowerPoints.

The skies over Donetsk made it clear: if you can’t crunch the numbers fast enough, you’re toast. The bureaucrats in Brussels are moving, but critics say they’re doing it with the speed and urgency of a garden snail at a union-mandated coffee break. The threat, unfortunately, doesn’t share their love of procedure. It arrives via quadcopter, costs $500, and sometimes drops grenades with all the grace of a piñata at a demolition derby.

The Red Sea Toll: Pirates, Premiums, and Pure Panic

Remember when the biggest shipping delay was someone mislabeling a crate in Rotterdam? Yeah, now it’s missiles in the Bab el-Mandeb.

Thanks to the Houthi rebels sinking merchant ships like it’s a bad Pirates of the Caribbean sequel, shipping insurers have cranked up their rates like a Roman emperor taxing wine. Several cargo carriers have now opted to take the “scenic” route around Africa—because what’s an extra two weeks between your IKEA sofa and civilizational collapse?

This isn’t just a naval headache—it’s a supply chain migraine. Longer voyages mean pricier goods, jittery markets, and the creeping realization that global trade can be derailed by one group with missiles and a grudge.

You don’t need to understand Yemeni tribal politics (and congratulations if you do), just know that a single strike near that narrow choke point could mean your holiday decorations cost double this year.

The Baltic’s Invisible Front: Now Starring Anchors as Weapons

Somewhere in the icy depths of Northern Europe, there’s a very naughty anchor pretending to be a guided missile.

Europe’s seabed—a chaotic knot of cables, pipelines, and extremely important underwater doodads—keeps having mysterious accidents. Finland and Sweden are investigating cable sabotage, and one particularly shady tanker allegedly played jump rope with multiple undersea lines.

This is “gray zone warfare”—the kind where no one wears uniforms, everyone denies everything, and the damage gets quietly billed to your electric company.

Just one “oops” down there can disrupt power, paralyze stock markets, or reroute half the internet. It’s like playing Operation, except the buzzer is a global recession.

Germany Rearms (No, Really This Time)

For decades, Germany treated defense like a gym membership—it paid for it, but rarely showed up.

That’s over. Berlin has smashed through NATO’s 2% spending ceiling like a Bavarian tourist at an all-you-can-eat schnitzel buffet. By 2029, it aims to hit 3.5% of GDP, which translates to tens of billions in tanks, missiles, and orders that ripple across European defense firms like a jackpot on a slot machine.

The reason? Putin reminded everyone that “just-in-time” logistics don’t mix well with tanks rolling through your neighbor’s yard.

But here’s what matters:

Coffee-Worthy Questions (Forget the Chamomile):

-

Will Europe deliver or just deliver speeches? It’s one thing to pass a budget. It’s another to actually build the stuff before 2042.

-

Who’s footing the bill—and will they faint when they see the tab? Germany’s finance ministry is now juggling debt rules and defense urgency like a flaming baton act.

-

What happens when Germany gets brawnier? NATO’s center of gravity shifts eastward: Poland becomes a logistics hub, the Baltics get a bigger shield, and France might start coughing politely at meetings.

Meanwhile, Ukraine continues testing all of this in real time—turning drones and electronic warfare into the ultimate DIY defense kit. The war has proven that brains, bandwidth, and a decent drone budget can sometimes outmaneuver sheer firepower.

Europe’s takeaway? You can’t spreadsheet your way out of an invasion—but you can try.

Want more breakdowns like this? Stick around. Next week we’ll be asking why a Greek island just bought more missiles than it has goats.

With access to C2 Financials’ 100+ lenders and decades of personal experience in building, turning around and managing companies, raising capital, and running M&A I can help provide solutions to maximize your operations and secure optimal funding.

858-229-7199 – jdevilliers@c2financial.com

Galley and Grit

How Not to Ruin the Turkey This Thanksgiving

(Or: How to Cook It Like a Danish Genius and a French Wizard, Without Losing Your Mind)

Ah, Thanksgiving. That magical time of year when we gather with loved ones, pretend to enjoy green bean casserole, and place a poultry beast roughly the size of a small car into the oven, hoping for a miracle.

But here’s the cruel joke of poultry: white meat and dark meat don’t play nicely in the oven. One cooks faster than the other, like a hare and a tortoise, except both end up dry if you don’t know what you’re doing.

I learned this the hard way—until I had the good fortune of cooking with Claus Meyer, co-founder of the culinary church known as Noma (yes, that Noma). Over a Danish Christmas goose—delicious, feathered relative of our American turkey—he shared the cardinal rule: Cook your bird in parts. That’s right. Take it apart. Give it therapy. Then cook it separately, reuniting the pieces like a warm family reunion right before serving.

Roast Like a Pro (Not a Pyromaniac)

Here’s how you cook the pieces so no one weeps into their gravy:

- White meat: Roast at 350°F for 16–20 minutes per pound, until the internal temp hits 165°F.

- Dark meat (legs & thighs): Roast at 325°F for 13–20 minutes per pound, until it reaches 180°F.

Once both are done, assemble like IKEA furniture (but with more joy), and toss the whole thing in a 300°F oven for 40 minutes to warm and crisp the skin. Voilà! Perfection.

Want to Go Full Turkey Nerd? Enter Sous Vide.

If you’re the sort who owns a kitchen blowtorch and knows what a shallot reduction is, you’re ready for this.

- Disassemble the turkey like a forensic pathologist. Breast meat in one Ziploc, dark meat in another.

- Add liquids and herbs:

- Breast: 1 cup sherry, plus bay leaf, rosemary, sage, and thyme.

- Dark meat: 1 cup port and the same herbal suspects.

- Sous vide setup:

- Breast: 55°C (131°F) for 18 hours

- Dark meat: 65°C (149°F) for 24 hours

After their spa treatment, refrigerate the bags until the big day. Then, reduce the cooking juices by half in a skillet until you’re left with liquid gold. That’s your gravy base. You’re welcome.

For the Overachievers: The Brining Saga

If you’re truly committed (or just avoiding relatives), why not start days earlier by brining the bird? According to Thomas Keller—the man behind The French Laundry and the reason culinary school dropouts cry into their saucepans—brining is the secret handshake of truly great turkey.

“Make a schedule,” Chef Keller says. “Brine. Air dry. Temper the bird.”

(Which sounds more like poultry boot camp than a holiday meal, but it works.)

Keller’s Brine Recipe:

- 1½ cups kosher salt

- 5 lemons, halved

- ½ cup honey

- 1 bunch each: thyme and parsley

- 2 bay leaves

- 2 garlic heads, halved crosswise

- 3 tbsp whole black peppercorns

- 6 quarts ice water

- 18–20 lb turkey, thawed

Instructions:

- Boil 4 quarts water with everything but the ice and turkey. Stir until salt dissolves.

- Add 6 quarts ice water. Let cool. (Unless you’re aiming for “Poached Thanksgiving.”)

- Submerge turkey in cooled brine. Refrigerate for 24 hours.

- Remove, pat dry, and let it air-dry uncovered in the fridge for another 24 hours.

- Roast. Shine. Accept compliments with fake modesty.

So whether you roast it, sous vide it, or brine it like a three-star general, the moral is this: Treat your turkey like royalty. It’s the centerpiece, not an afterthought. You’ve got one job—don’t mess it up.

Happy Thanksgiving. May your bird be juicy, your gravy rich, and your relatives moderately tolerable.

Need a steady hand?

Free consult for strategy. Free consult for capital. Clear options, zero pressure.

Moral Compass

Photo by Giulia Bertelli on Unsplash

Gratitude, On Purpose

Martin Seligman didn’t invent happiness—he just dragged it into the lab, strapped it to a chair, and asked it politely (and repeatedly) to stop squirming. His pivot from learned helplessness to Positive Psychology gave us PERMA: Positive emotion, Engagement, Relationships, Meaning, Accomplishment. Five fine pillars of flourishing. But here’s the kicker—gratitude is the quiet crankshaft that drives them all.

Gratitude brightens mood, sharpens focus on what’s working, strengthens human ties, adds depth to meaning (you don’t just get gifts—you notice the giver), and fuels effort without turning you into a burned-out husk. In other words, it’s not just nice—it’s necessary.

Seligman’s top tools aren’t high-tech. They’re the psychological equivalent of duct tape: simple, cheap, surprisingly effective.

-

Three Good Things: Every night, write down three things that went well and why.

-

The Gratitude Letter: Write to someone you never thanked properly. Bonus points if you read it to them—out loud, face to face, without fleeing the room.

These two micro-habits are clinically shown to reduce anxiety, buffer depression, and boost life satisfaction. Why? Because gratitude retrains your brain’s spotlight—from “everything is on fire” to “some things are working.” It shifts your inner monologue from “I’m doomed” to “I’ve had help.” It reminds you that you’re not a lone soul screaming into the void.

But here’s where things get inconvenient.

Humans are incurable goal-chasers. We orbit whatever we decide is ultimate: success, family, health, reputation, recognition. And when we finally catch the prize? It shapeshifts. The job wasn’t enough. The house needs a second story. The kids, for some reason, still don’t send thank-you cards.

Gratitude interrupts that cosmic hamster wheel. It doesn’t kill ambition; it just puts it on a leash.

But it also elbows us into a question Positive Psychology—by design—doesn’t answer for you:

What’s the point of all this?

Not the Monty Python answer (brilliant film, terrible strategy), but the real one. If life is a fluke—cosmic soup gone slightly sentient—then sure, pass the appetizers and enjoy the serotonin. Hug your people. Savor your coffee. Keep your gratitude list tidy to help your amygdala behave.

But—if you believe there’s a Creator, the equation changes. Gratitude isn’t spiritual flattery, as if God runs on Yelp reviews. It’s spiritual formation. A reshaping. A training ground for holding gifts without being owned by them.

That’s why Scripture’s relentless refrain—give thanks in all circumstances—isn’t cosmic customer service. It’s spiritual muscle-building. Seligman would say (and research backs it up): gratitude is good for you. Not in a smug, wellness-journal kind of way—but in a grit-and-grace, trench-deep way. It widens your lens, calms your nerves, weaves stronger ties, and keeps you standing when life throws knees to the ribs.

Your November Playbook:

-

Run a 7-day “Three Good Things” sprint—do it yourself or with your team. At the end, ask: What patterns emerged?

-

Write a Gratitude Letter—and if you can, read it aloud. Yes, it may feel awkward. Yes, it’s often unforgettable.

-

Ask the big one: What do you believe about a Creator? And what’s your “Ultimate”?

Gratitude won’t make life easier. But it will stretch your soul’s capacity—to work, to love, to suffer well, and to notice who stood by you.

Which brings us to the real question this Thanksgiving:

What are you grateful for—and what does that say about what you believe life is ultimately for?

From our friends at Dispair.com

Stuck at the helm? Let’s chart the next move.

If your business is wrestling with growth, team, or cash-flow puzzles—or you’re weighing how to fund the next big step—bring me your mess. I’ll bring a map.

Two simple, no-pressure ways to start:

-

Free Coaching Consultation

A focused 20–30 minutes to assess what’s blocking momentum and sketch 2–3 practical plays you can run this month. -

Free Capital Options Call

If you need financing for a new purchase, a refi, or a life event, we’ll review current options and model what’s smart—not just what’s available.

No jargon. No hard sell. Just clear ideas from someone who’s been in the wheelhouse when the water wasn’t calm.

Ready?

Chart a Coaching Call —or— Explore Capital Options +18582297199

Prefer email? Send a quick note to [jdevilliers@c2financial.com] with “Let’s talk” in the subject, and tell me what you’re navigating.

General Disclosure

This publication is for informational and educational purposes only and reflects the personal opinions of the author as of the date of publication. The views expressed do not necessarily reflect the views of any employer, client, or affiliated organization. The author is not selling, brokering, or offering any securities, investments, insurance, or other financial products through this publication.

No Professional Advice. Nothing herein is legal, tax, investment, accounting, or other professional advice. You should consult your own qualified advisors before making any decision.

No Recommendation or Solicitation. References to companies, markets, instruments, or strategies are illustrative and not recommendations, offers, or solicitations to buy or sell any product or service.

Sources and Accuracy. Some content summarizes or links to third-party sources believed to be reliable; however, the author does not warrant the completeness, timeliness, or accuracy of any information and assumes no responsibility for errors or omissions. Markets and laws change—information may become outdated without notice.

No Duty to Update. The author has no obligation to update any content, even if subsequent events make statements inaccurate.

Performance and Risk. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

No Client Relationship. Reading or interacting with this publication does not create a client, advisory, or fiduciary relationship with the author or [Your Company Name].

Third-Party Links. Links are provided for convenience and do not constitute endorsements. The author is not responsible for third-party content or policies.

Conflicts & Affiliations. The author may hold positions or have business relationships relevant to topics discussed and will endeavor to disclose material conflicts where appropriate.

© 2025 Johann de Villiers. All rights reserved. Contact: jdevilliers@C2Financial.com .

This licensee is performing acts for which a real estate license is required. C2 Financial Corporation NMLS #135622 is licensed by the California Department of Real Estate, Broker # 01821025; Arizona Department of Financial Institutions, Broker # 919209; Colorado Division of Real Estate; Florida Office of Financial Regulations, OFR# MBR3519; Tennessee Department of Financial Institutions, DFI# 135622; Washington Mortgage Broker License MB-135622. Loan approval is not guaranteed and is subject to lender review of information. All loan approvals are conditional, and all conditions must be met by borrower. Loan is only approved when lender has issued approval in writing and is subject to the Lender conditions. Specified rates may not be available for all borrowers. Rate subject to change with market conditions. C2 Financial Corporation is an Equal Opportunity Mortgage Broker/Lender. The services referred to herein are not available to persons located outside the state of CA, AZ, CO, FL, TN and WA.

Johann de Villiers NMLS # 71252, CA DRE # 01746466, AZ #1040617, CO # 100534343,

FL #LO111486, TN # 71252, WA # MLO-71252

Related Posts