Issue #7 - April 2026 North Star Briefing sails where headlines meet consequences. This issue charts the…

North Star Briefing January 2026

ISSUE # 4 – January 2026

Editor’s Note

This month:

-

2026 won’t be about whether the Fed cuts. It’ll be about whether investors believe the Fed is cutting for the right reasons;

-

The winners in housing in 2026 won’t be the loudest; they’ll be the most prepared — pre-underwritten, numbers-first, and ready to move when the right opportunity finally blinks;

-

Bottom line: the big affordability shock is mainly a 2020–2024 story, especially in housing;

-

The Noriega Precedent (a.k.a. “History Doesn’t Repeat, But It Does Copy-Paste”);

-

“Remember: the goal isn’t perfection. It’s fewer ‘surprise calories’ and more days where you’re the captain—not the Oreo.”

-

The goal isn’t to feel nothing. The goal is to stop pretending we’re God.

- Trump’s Ax and the rotten tree.

Need a steady hand?

I help bankable-but-not-bank-shaped clients identify and fix the root problem—then fund the right solution.

-

-

Rate Radar -The Next Fed Chair: Markets Are Calm, Which Is How You Know They’re Nervous

-

Harbor Report – Price Cuts, Condo Blues, and Why “Crash” Keeps Missing Its Appointment

-

Stateside Signals –The Great American “Affordability” Panic (Now With Actual Numbers)

-

Open Seas Outlook – Maduro: Indictments, “Cartels,” and the World’s Most Awkward Custody Dispute

-

Galley & Grit – “New Year – New Year’s Reso”… Until an Oreo Looks at You Funny

-

Moral Compass – Anxiety: The Official Emotion of Modern Life

-

Beacon in the Storm – Trump and the Deep State

-

Ready to move? Free coaching consult or capital options—your call.

858-229-7199 – jdevilliers@c2financial.com

Rate Radar

“2026 won’t be about whether the Fed cuts. It’ll be about whether investors believe the Fed is cutting for the right reasons.”

Need clarity?

I help find the strategy that earns its financing: address the problem, then fund what works.

Harbor Report

Price Cuts, Condo Blues, and Why “Crash” Keeps Missing Its Appointment

If you listen to housing chatter long enough, you’ll hear the same prophecy delivered with the confidence of a man selling end-times pamphlets: “The big crash is coming any day now.” And yes—some sellers are finally learning that “I saw my neighbor list for $X” is not a pricing strategy, it’s a bedtime story.

The data backs up the mood shift. The Wall Street Journal, citing NAR, reported that 57% of homes sold in 2025 through October had at least one price cut—which is another way of saying: a lot of sellers tried “aspirational pricing,” met “aspirational demand,” and then blinked. The Wall Street Journal Realtor.com’s October 2025 report shows 20.2% of active listings had price reductions, elevated by recent standards and flirting with levels last seen back in 2017. Realtor Translation: the market is no longer a bidding-war mosh pit; it’s becoming a negotiation again. Bring a helmet.

But here’s the twist: price cuts are not the same thing as a collapse. They’re often just the market shaving off the froth—especially in places that got a bit too giddy in 2021–2022.

Where things do look properly rough is condos. A WSJ report in early January 2026 notes condo prices were down 1.9% year-over-year in September and October 2025, the biggest annual drop since 2012, with buyers spooked by rising HOA dues (insurance and maintenance are doing their own inflation cosplay) and softer demand. The Wall Street Journal+1 In some metros, a painful share of condos are now worth less than their prior sale—especially where supply is heavy and the HOA math is ugly. The Wall Street Journal Single-family homes, meanwhile, have generally held up better, helped by limited inventory and owners who simply refuse to sell unless bribed with a sub-4% mortgage.

That “owners have equity” point matters. Zillow reported in November 2025 that only about 4.1% of homes were worth less than their last sale price—a small, but rising, slice. Zillow+1 That’s not nothing, but it’s also not 2008, when negative equity and forced selling turned a slowdown into a bonfire.

Which brings us to Bill McBride at Calculated Risk—one of the few people who waved the red flag in 2005 and got it right. In a 2005 post, he highlighted household mortgage debt as a percent of GDP as a key warning sign. The updated versions of that chart (now running through 2025-era data) tell a different story: today’s cycle doesn’t show the same mortgage-debt-fueled bubble profile, and McBride’s “bottom line” remains that we’re unlikely to see cascading price declines driven by distressed sales the way we did last time. calculatedrisk.substack.com+1

So what should we expect in 2026? Not a crash-by-default. More likely: pockets of correction (especially where inventory is up and demand is softer), a messy condo segment, and a broader market that slows and grinds rather than implodes—creating real opportunities for buyers and investors who like negotiating more than competing in auction theater.

In other words: less “housing apocalypse,” more “housing hangover.” Still unpleasant, but survivable—with ibuprofen and a calculator.

This isn’t 2008’s sequel. It’s a different genre: fewer foreclosures, more bargaining, and a condo market that’s currently asking for a therapist and a stiff drink.

The upside for homebuyers is simple: when sellers start cutting prices and days-on-market stretch out, you get something we haven’t seen in a while — leverage. Inspections come back, credits reappear, and “no contingencies” stops being the required blood oath.

For investors, a cooler market is where deals start acting like deals again: better entry points, more realistic seller expectations, and the ability to negotiate terms instead of sprinting into offers like it’s a Black Friday stampede.

The winners in 2026 won’t be the loudest; they’ll be the most prepared — pre-underwritten, numbers-first, and ready to move when the right opportunity finally blinks.

Ready to move? Walk out of our first consultation with a 3-step plan that makes financing optional, realistic—and powerful when used.

With access to C2 Financials’ 100+ lenders and decades of personal experience in building, turning around and managing companies, raising capital, and running M&A I can help provide solutions to maximize your operations and secure optimal funding.

858-229-7199 – jdevilliers@c2financial.com

Stateside Signals

Pueblo Independent News

The Great American “Affordability” Panic (Now With Actual Numbers)

By early 2026, affordability is the word everyone is waving around like a political foam finger. Except the foam finger costs $19.99 now, plus a “convenience fee,” plus an emotional support tip screen.

Let’s defuse the rhetoric and look at when the unaffordability actually happened.

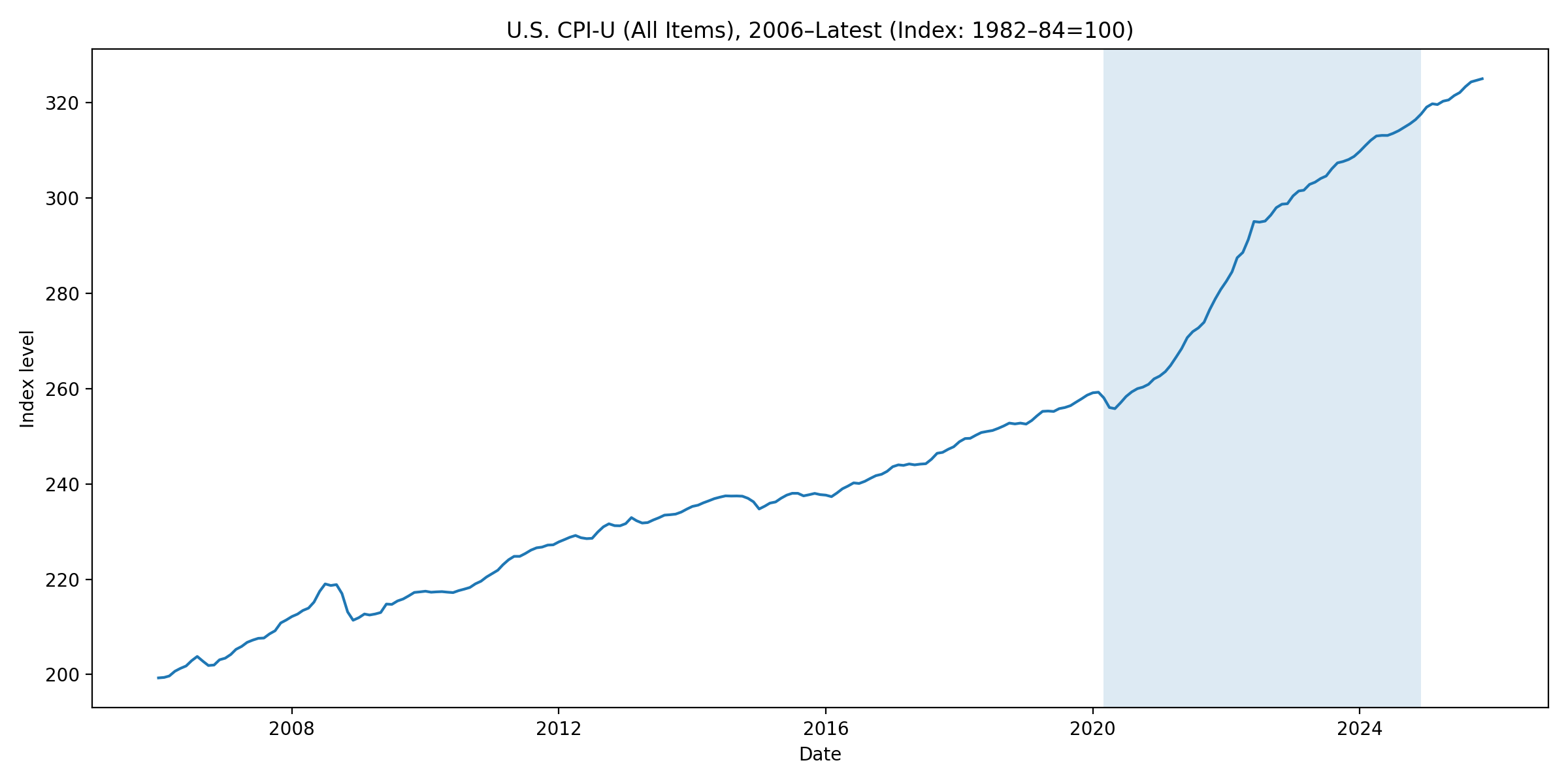

First: overall prices. The Consumer Price Index (CPI-U) spent 2006–2020 doing its usual “slow creep” thing — the economic equivalent of your cat gradually pushing a glass off the counter. Annoying, predictable, and generally inside the Fed’s comfort zone. Then the pandemic hit and CPI stopped creeping and started sprinting like it’d seen a cucumber. From December 2019 to December 2024, CPI rose about 22.8%.

“This is the moment ‘temporary’ inflation stopped being temporary and started applying for squatter’s rights.”

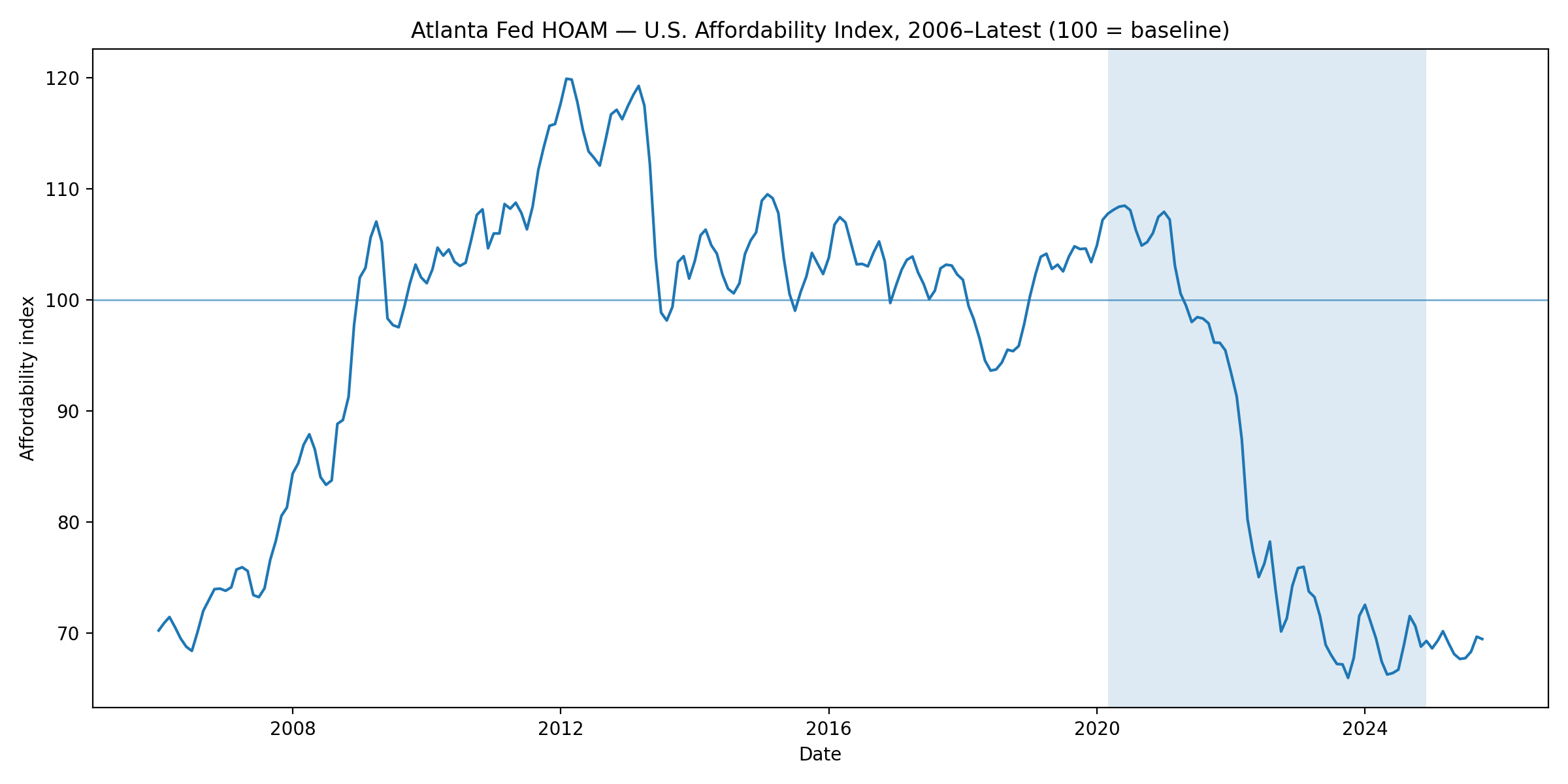

Second: housing affordability. This is where the pain gets personal. Even if your grocery bill is irritating, housing is the thing that makes people start saying sentences like, “Maybe I’ll just live in a tasteful shed.” The Atlanta Fed’s HOAM affordability index shows the shift brutally: affordability didn’t just “worsen,” it fell off a cliff as home prices surged and mortgage rates later rose. From January 2020 to December 2024, the HOAM affordability index dropped about 33.9% (lower = less affordable). Federal Reserve Bank of Atlanta+1

“If 100 is ‘affordable,’ we spent 2022–2024 exploring the concept of ‘no, actually’ in great detail.”

“If 100 is ‘affordable,’ we spent 2022–2024 exploring the concept of ‘no, actually’ in great detail.”

Now the “how is it changing?” part — because doom is not a strategy.

The good news is inflation has cooled from its peak, and by late 2025 real wages were back to growing modestly again: BLS reported real average hourly earnings up 0.8% from Nov 2024 to Nov 2025. Bureau of Labor Statistics and gas prices are way down! That doesn’t undo the price level jump (those prices are still up there, living their best life), but it does mean paychecks have stopped losing the race as badly.

Bottom line: the big affordability shock is mainly a 2020–2024 story, especially in housing. The path out is slower: wages catching up, rates and supply doing whatever mysterious ritual they do, and politics pretending it was all caused by the other team’s choice of breakfast cereal.

Need a steady hand?

I help bankable-but-not-bank-shaped clients identify and fix the root problem—then fund the right solution.

Open Seas Outlook

Photo CNN

With access to C2 Financials’ 100+ lenders and decades of personal experience in building, turning around and managing companies, raising capital, and running M&A I can help provide solutions to maximize your operations and secure optimal funding.

858-229-7199 – jdevilliers@c2financial.com

“New Year – New Year’s Reso”… Until an Oreo Looks at You Funny

January is the month of sacred vows. This is the year we become healthier, wiser, wealthier—possibly also taller, more photogenic, and mysteriously immune to temptation. We write plans. We buy gear. We announce to friends (a classic tactical error). We’re going to eat clean, lift heavy, read books with intimidating subtitles, learn a foreign language, meditate, hustle, and—why not—develop abs that could deflect small arms fire.

Then mid-January arrives and real life wanders in like an uninvited houseguest wearing muddy boots: work deadlines, family stuff, weather, stress, and that strange phenomenon where the couch becomes gravitationally stronger after 7 p.m. By February, our routine has the structural integrity of wet tissue paper. By the end of February, the only thing we’re consistently lifting is the remote. We promise ourselves: next year will be the year. This year was simply ambushed by “unforeseen circumstances,” like Tuesdays.

Health resolutions usually go first because they’re the most honest. Exercise is great—truly—but the scale can be an emotional terrorist. You start working out and suddenly your weight doesn’t drop, or it even bumps up a little. That’s not because your body is “turning fat into muscle” (sadly, biology doesn’t do alchemy). It’s because muscle is denser than fat, and early training can add muscle and water retention while fat loss quietly gets on with its job. The mirror improves, your pants fit better, and the scale sits there like a smug accountant saying, “I’m not impressed.”

And then there’s the food math. Weight loss is mostly won in the kitchen—because it turns out you can’t outrun your fork. Also, the calories in “just one Oreo” can make an hour on the treadmill feel like you paid off a mortgage by finding a quarter under the sofa cushion. And who can have only one Oreo? Sociopaths, that’s who.

Enter the newest plot twist: AI meal analysis apps. Yes, you can now take a photo of your plate—even in a restaurant—and your phone will do its best to estimate calories, protein, carbs, fat, and sometimes extras like sugar and sodium. It’s like having a tiny dietitian living in your camera… with the social grace of a spreadsheet.

One warning: these apps usually ask you to confirm what they see. This is an excellent character-building moment, especially if you’ve already “tested” three fries for quality control before you took the picture. Be honest. The AI already suspects you.

Here are the crowd favorites:

-

MyFitnessPal (Meal Scan) — the household name with camera-based recognition

-

Lose It! (Snap It) — photo logging plus macro tracking

-

MyNetDiary (AI Meal Scan) 100M+ downloads on Google Play — deeper nutrient nerdiness (they brag about a lot of nutrients)

-

Foodvisor — built for “photo first,” with nutrition breakdown + coaching

-

SnapCalorie — the lab-coat option; on some iPhones it can estimate volume using depth

Best part? It turns dieting into a weird little video game: points, streaks, progress bars, and the occasional boss battle called “Dinner Out.” And who knows—if your phone starts keeping score, you might just carry that New Year streak all the way into March… like a legend.

“Remember: the goal isn’t perfection. It’s fewer ‘surprise calories’ and more days where you’re the captain—not the Oreo.”

Need a steady hand?

Free consult for strategy. Free consult for capital. Clear options, zero pressure.

Moral Compass

“The goal isn’t to feel nothing. The goal is to stop pretending we’re God.”

In the New Yorker, Jill Lepore surveyed the destruction of the Trump administration’s first three months: “Trump felled so much timber not because of the mightiness of his ax but because of the rot within the trees and the weakness of the wood.”

Stuck at the helm? Let’s chart the next move.

If your business is wrestling with growth, team, or cash-flow puzzles—or you’re weighing how to fund the next big step—bring me your mess. I’ll bring a map.

Two simple, no-pressure ways to start:

-

Free Coaching Consultation

A focused 20–30 minutes to assess what’s blocking momentum and sketch 2–3 practical plays you can run this month. -

Free Capital Options Call

If you need financing for a new purchase, a refi, or a life event, we’ll review current options and model what’s smart—not just what’s available.

No jargon. No hard sell. Just clear ideas from someone who’s been in the wheelhouse when the water wasn’t calm.

Ready?

Chart a Coaching Call —or— Explore Capital Options +18582297199

Prefer email? Send a quick note to [jdevilliers@c2financial.com] with “Let’s talk” in the subject, and tell me what you’re navigating.

General Disclosure

This publication is for informational and educational purposes only and reflects the personal opinions of the author as of the date of publication. The views expressed do not necessarily reflect the views of any employer, client, or affiliated organization. The author is not selling, brokering, or offering any securities, investments, insurance, or other financial products through this publication.

No Professional Advice. Nothing herein is legal, tax, investment, accounting, or other professional advice. You should consult your own qualified advisors before making any decision.

No Recommendation or Solicitation. References to companies, markets, instruments, or strategies are illustrative and not recommendations, offers, or solicitations to buy or sell any product or service.

Sources and Accuracy. Some content summarizes or links to third-party sources believed to be reliable; however, the author does not warrant the completeness, timeliness, or accuracy of any information and assumes no responsibility for errors or omissions. Markets and laws change—information may become outdated without notice.

No Duty to Update. The author has no obligation to update any content, even if subsequent events make statements inaccurate.

Performance and Risk. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

No Client Relationship. Reading or interacting with this publication does not create a client, advisory, or fiduciary relationship with the author or [Your Company Name].

Third-Party Links. Links are provided for convenience and do not constitute endorsements. The author is not responsible for third-party content or policies.

Conflicts & Affiliations. The author may hold positions or have business relationships relevant to topics discussed and will endeavor to disclose material conflicts where appropriate.

© 2025 Johann de Villiers. All rights reserved. Contact: jdevilliers@C2Financial.com .

This licensee is performing acts for which a real estate license is required. C2 Financial Corporation NMLS #135622 is licensed by the California Department of Real Estate, Broker # 01821025; Arizona Department of Financial Institutions, Broker # 919209; Colorado Division of Real Estate; Florida Office of Financial Regulations, OFR# MBR3519; Tennessee Department of Financial Institutions, DFI# 135622; Washington Mortgage Broker License MB-135622. Loan approval is not guaranteed and is subject to lender review of information. All loan approvals are conditional, and all conditions must be met by borrower. Loan is only approved when lender has issued approval in writing and is subject to the Lender conditions. Specified rates may not be available for all borrowers. Rate subject to change with market conditions. C2 Financial Corporation is an Equal Opportunity Mortgage Broker/Lender. The services referred to herein are not available to persons located outside the state of CA, AZ, CO, FL, TN and WA.

Johann de Villiers NMLS # 71252, CA DRE # 01746466, AZ #1040617, CO # 100534343,

FL #LO111486, TN # 71252, WA # MLO-71252

Related Posts