Issue #7 – April 2026

Issue #7 – April 2026

ISSUE # 6 - March 2026 Editor's Note This month: Is 5.98% the start of…

North Star Briefing – April 2026

North Star Briefing sails where headlines meet consequences. This issue charts the mortgage rate swings, a Japanese interest in building US housing, the effect of the Gig economy on the labor market, the unexpected scale of the war in Iran, the curious choice of the Easter ham, the cost of standing up for your convictions and the event that changed the world.

-

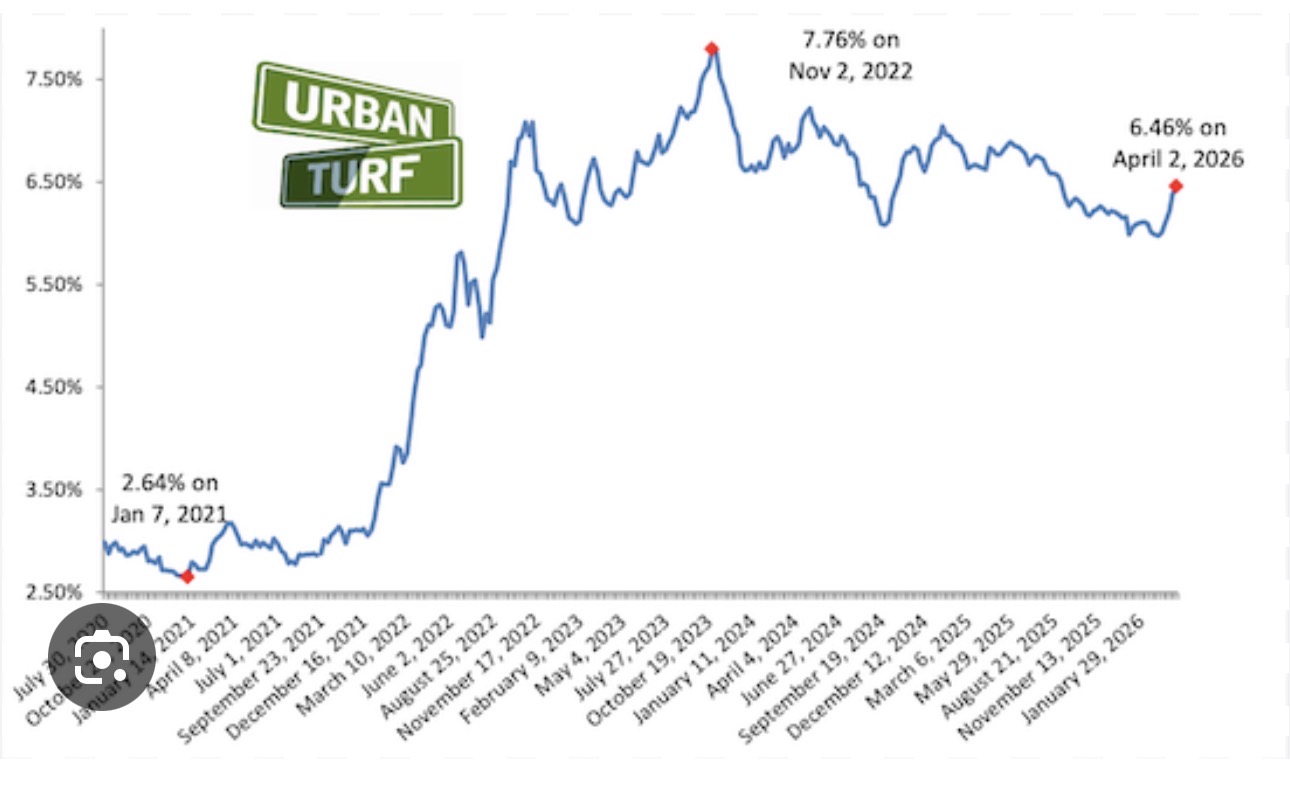

Rate Radar – So… was it spring, or just one very confused swallow?

-

Harbor Report – Japan Goes House-Hunting in America (and the “Smart Money” Isn’t Laughing)

-

State Side Signal – America’s Gig Economy: the labor market that keeps slipping off the clipboard

-

Open Seas Outlook – Iran: Persia’s Long Shadow, a Modern Tragedy, and the Awkward Return of the Crown

-

Galley & Grit – The Easter Ham: How Did We End Up Eating the “Wrong” Animal?

-

Moral Compass – Joseph of Arimathea: The Quiet Courage of Showing Up When It Costs You

-

Beacon in the Storm – The event that changed the world.

Need a steady hand?

I help bankable-but-not-bank-shaped clients identify and fix the root problem—then fund the right solution.

So… was it spring, or just one very confused swallow?

Japan Goes House-Hunting in America (and the “Smart Money” Isn’t Laughing)

If you’ve felt like U.S. homebuilders have been quietly upgraded from “cyclical headache” to “strategic national asset,” you’re not imagining it. A fresh wave of Japanese homebuilder acquisitions is turning the U.S. housing market into something that looks… suspiciously like a long-term investment thesis.

And yes—this comes right on the heels of Berkshire Hathaway’s highly publicized toe-dip into U.S. homebuilders, which is about as subtle as Warren Buffett doing cartwheels in a top hat.

The new storyline: Japanese builders are buying American builders—fast

Multiple reports now point to a sustained buying spree:

- Since 2020, Japanese builders have announced or completed 23 acquisitions of U.S. single-family homebuilders—more than double the number from 2013–2019.

- Collectively, they’re projected to control around ~6% of the U.S. home-construction market.

That’s no longer “dipping a toe in the pool.” That’s buying the pool house and asking where you keep the chlorine.

The headline deals (the kind you can’t ignore)

This isn’t just small bolt-on buying. It’s multi-billion-dollar consolidation:

- Sumitomo Forestry → Tri Pointe Homes: announced Feb 13, 2026, an all-cash deal at $47/share, valuing the transaction at about $4.5B.

- Sekisui House → M.D.C. Holdings: announced earlier (Jan 2024) at roughly $4.95B—a deal that would vault Sekisui into the top tier of U.S. builders by volume.

- Daiwa House (via Trumark/Stanley Martin platform) has continued to expand through acquisitions, including Trumark’s move into the Pacific Northwest via JK Monarch (Mar 2026).

- And in the “not huge, but strategically meaningful” category: Daiwa’s U.S. platform Stanley Martin agreed to acquire United Homes Group for an enterprise value of $221M (Feb 2026), expanding its footprint and lot pipeline.

Why Japan is doing this (hint: demographics is destiny)

Japanese homebuilders aren’t buying the U.S. because they suddenly fell in love with American zoning boards (nobody loves American zoning boards). They’re doing it because Japan’s domestic housing runway is shrinking—aging population, fewer households forming, long-term demand constraints. The U.S., by contrast, still has household formation, migration, and chronic under-supply.

In other words: Japan is not “chasing a hot market.” Japan is escaping a cold one.

Why the U.S. is attractive even with higher rates

From a U.S. perspective, this is happening during a period that should scare away buyers of builders: higher mortgage rates, affordability pressure, and uneven demand.

And yet Japanese firms see long duration value:

- The U.S. market is enormous relative to Japan’s and still structurally underbuilt.

- Some Japanese buyers can access capital at different costs than U.S. competitors, and they’re often willing to play a longer game.

- They also bring process and manufacturing know-how (including more industrialized building methods), which matters when labor is constrained and cycle volatility is high.

“Smart money” signals: Buffett’s builder bets (and what they really mean)

Now to the fun part: Berkshire Hathaway.

In mid-2025, Berkshire disclosed new stakes in Lennar and D.R. Horton—moves widely read as a bullish signal for the homebuilding complex.

To be clear: Berkshire later trimmed/closed the D.R. Horton position and added to Lennar, which suggests this isn’t a simplistic “builders only go up” bet—it’s a selective one.

But here’s the important takeaway: Buffett-world didn’t buy homebuilders because it expects 2.75% mortgages tomorrow morning. It bought because it sees enduring demand, supply constraints, and builders as the marginal supplier in a country that can’t print houses.

What this could mean for the housing market (not tomorrow—over years)

This acquisition wave matters because it can impact the market’s “production capacity”:

- More capital + stronger balance sheets can keep building going during downcycles.

- Lot pipelines and land strategy get consolidated and professionalized.

- Operational efficiency can improve, which may help affordability at the margin (not miracles—margins).

- Over time, increased new-home production is one of the few real mechanisms that can relieve price pressure without requiring a recession to do the job.

That said: the U.S. housing market is still bottlenecked by permits, zoning, labor, and infrastructure. So this isn’t “prices crash next quarter.” It’s more like: prices face stronger gravity over the next several years if supply capacity grows meaningfully.

Why this matters to investors and builders (and yes, to financing)

If Japanese builders are building a bigger U.S. footprint while Berkshire is selectively backing large builders, here’s the implication:

- The next cycle may reward operators: builders with disciplined land positions, scalable processes, and financing strategies that can survive higher-for-longer rates.

- For real estate investors, it may create opportunities in infill, build-to-rent adjacency, value-add near new supply corridors, and “who controls the dirt” plays.

And for your corner of the world: when builders expand and consolidate, they need capital stacks that actually work—construction lines, spec financing, takeout strategies, DSCR rentals, and bridge-to-perm structures that don’t collapse if rates refuse to cooperate.

Bottom line

Japan isn’t buying U.S. builders because the U.S. is easy. Japan is buying because the U.S. is still growing, still underbuilt, and still the world’s most liquid sandbox for housing-scale expansion.

And when you see that kind of strategic buying—alongside Berkshire’s builder exposure—you don’t have to assume the market is about to boom.

You only have to conclude this:

The people with patient money think U.S. homebuilding matters more than the headlines imply

America’s Gig Economy: the labor market that keeps slipping off the clipboard

Rana Foroohar’s point in the FT is deceptively simple: the labor market looks “weird” because more work is happening outside the neat little boxes our statistics were built to count. Payroll growth (formal jobs) has been soft, but unemployment claims haven’t risen the way you’d expect—while new business applications have surged to record highs. That combination makes more sense if a growing share of people are shifting into freelance/contract work instead of showing up as “unemployed.”

The gig economy isn’t just Uber anymore

The Federal Reserve’s own household survey shows how broad this has become. In 2024, 13% of adults made money selling things (resale/gig), and 9% made money doing short-term tasks like rides, deliveries, or odd jobs—about 22% doing at least one of these activities.

And it’s not only at the lower end. The MBO Partners “State of Independence” report finds 5.6 million independent workers earned $100k+ in 2025. That’s a lot of “consultant” business cards—and a lot of income that doesn’t look like W-2 payroll.

Why the data feels contradictory

FT quotes (via TS Lombard’s Steve Blitz) a key mechanism: tech lowered the barrier to entry for everything from retail selling to professional services—meaning layoffs in corporate roles can translate into “employee → consultant” rather than “employee → unemployment line.”

So the labor market can cool while the consumer keeps spending—because people are still earning, just in ways that don’t show up cleanly in traditional measures.

The cost of “freedom”: anxiety and a thinner safety net

Here’s the darker side Foroohar highlights: independence can mean no paid time off, no employer healthcare, no employer retirement plan—you fund your own life raft.

And it helps explain why sentiment is sour even when top-line unemployment isn’t screaming. Gallup found only 28% of U.S. workers said it was a good time to find a quality job (Q4 2025); among college-educated workers, it was 19%.

Layer in another uncomfortable stat: St. Louis Fed research finds that for non-white family heads born in the 1980s, the wealth “college premium” is statistically indistinguishable from zero—meaning the degree doesn’t reliably translate into wealth-building the way it did for prior generations.

Why this matters for markets (and for mortgages)

Consumer spending is roughly two-thirds of GDP (about 68% recently), so an economy that’s increasingly “gig-shaped” can stay resilient… right up until insecurity makes people slam the brakes on spending.

And for housing finance, this is the big practical point: the American worker is becoming less W-2 shaped. That doesn’t mean “less qualified.” It means income is more likely to be 1099, contract, consulting, self-employed, multi-stream, and sometimes irregular month-to-month.

Which is exactly why Non-QM isn’t some niche oddity anymore—it’s becoming the bridge between:

- how people actually earn, and

- what the traditional mortgage box still wants to see.

Moral of the story

America’s gig economy is both entrepreneurial and precarious—a land of opportunity where your benefits package is basically “good luck.” If policymakers want stability without choking flexibility, they’ll eventually have to wrestle with benefits portability and safety-net design.

In the meantime, don’t be surprised if the labor market keeps sending “mixed signals.” It may not be confused. It may just be evolving faster than the scoreboard.

Iran: Persia’s Long Shadow, a Modern Tragedy, and the Awkward Return of the Crown

Iran—ancient Persia’s heir—isn’t some “new problem.” It’s one of the great civilizations of history, and its story is intertwined with Israel’s in ways most modern headlines conveniently forget (Cyrus, Esther, exile, return). But the last century reads less like epic poetry and more like a political cautionary tale: foreign intervention, authoritarian modernization, secret police, revolution, theocracy, and now open war. The moral question hovering over all of it: what comes next—and who pays for the answer?

Persia and Israel: a long memory

Before we race into the last 100 years, it’s worth remembering: “Persia” isn’t merely a geopolitical adjective. In the biblical story, Persian rulers loom large—most famously Cyrus, associated with allowing Jewish exiles to return and rebuild.

That shared history doesn’t erase today’s conflict, but it does complicate the lazy idea that Iran and Israel are “eternal enemies.” History is messier—and more human—than slogans.

1953: The coup that never really ended

Modern Iran’s trajectory pivots hard in 1953, when Prime Minister Mohammad Mosaddegh was overthrown in a coup supported by U.S. and British intelligence (CIA/MI6)—the episode often tied to fears of Soviet influence and the struggle over oil.

Important precision: the Shah (Mohammad Reza Pahlavi) already held the throne, but the coup strengthened his rule and burned a long-lasting lesson into Iranian political memory: the West will preach democracy, and then quietly sabotage it when inconvenient.

It’s hard to build trust on that foundation. Even harder to rebuild it once it cracks.

The Shah: modernization with a boot on the neck

The Shah’s era brought real modernization—but also escalating repression. His intelligence service, SAVAK, became notorious enough that even U.S. diplomatic records from the 1970s reflect recurring controversy about violence and political prisoners.

So yes, the Shah was “pro-West.” But “pro-West” is not the same as “pro-freedom.” Many Iranians experienced the monarchy as a bargain where the price of stability was fear.

And fear always collects interest.

1979: Revolution… then the revolution turns inward

The 1979 revolution overthrew the monarchy and established the Islamic Republic. Many Iranians initially hoped for dignity and justice after corruption and repression. But the new regime soon developed its own coercive machinery—restricting speech, criminalizing dissent, and punishing opposition. Amnesty’s reporting describes ongoing suppression of expression and peaceful assembly, alongside extensive arbitrary detention and systemic abuses.

This is the recurring tragedy of modern revolutions: the crowd celebrates freedom… and then discovers the new rulers also enjoy being unaccountable. It’s like replacing a broken lock with a stronger lock—on the outside.

Iran’s regional strategy: proxies, partners, and perpetual confrontation

Iran’s leaders have pursued influence through a network of allied militias and political movements across the region. The U.S. has designated Iran a State Sponsor of Terrorism since 1984, and State Department reporting describes support to groups such as Hezbollah and others.

April 2026: war expands, the Gulf gets nervous, and Hormuz becomes the world’s choke point

In this current conflict cycle, reporting indicates the war began after U.S. and Israeli strikes on Iran (late February), followed by Iranian retaliation including attacks on Israel and Gulf Arab states, with serious disruption tied to the Strait of Hormuz and regional shipping.

Whatever your politics, one fact is stubborn: when Hormuz is unstable, the world feels it—in fuel prices, inflation, and the emotional health of everyone who commutes.

“Long live the Shah”… really?

One of the most arresting developments is that some Iranians—especially in parts of the diaspora—have rallied around Reza Pahlavi, the Shah’s son, as a symbolic alternative to the Islamic Republic. Reuters has reported on his efforts to position himself as a national figure amid expanding protests and calls for change.

Why would anyone want a return of anything associated with the Shah era, given SAVAK and repression?

Because when people are desperate, they don’t always reach for perfect options. They reach for alternatives that feel imaginable:

- a symbol of “pre-theocratic Iran,”

- a hope (rightly or wrongly) for a constitutional monarchy rather than a police state,

- or simply the brutal logic of “anything but this.”

That doesn’t mean the majority wants a monarchy. It means the regime’s legitimacy has eroded enough that old symbols start looking new again.

The West, morality, and the limits of export

Here’s where Americans (and Europeans) should practice humility—an endangered virtue.

The West often speaks as if it has a monopoly on the good life and the pathway to peace. History doesn’t support that confidence. And trying to “install” Western values in societies with different histories, religious structures, and power networks often goes sideways—even when the values themselves are admirable.

Which raises the question that makes regime-change plans so fragile:

How many Iranians genuinely support the Islamic Republic’s model—

and how many tolerate it because fear, fragmentation, or lack of trusted alternatives makes change feel worse?

When outsiders don’t know the answer, they tend to get “regime change” wrong in exactly the same way—every time.

Closing thought

Iran is not a cartoon villain, and it’s not a simple liberation story either. It’s a great civilization with real grievances, real internal divisions, and real people caught between state repression, war, and ideology.

It’s easy to argue about Iran as a concept. It’s much harder—and more important—to remember Iranians as people.

The Easter Ham: How Did We End Up Eating the “Wrong” Animal?

Joseph of Arimathea: The Quiet Courage of Showing Up When It Costs You

We live in a time where “courage” is often confused with posting the right sentence on the internet. Joseph of Arimathea offers a very different kind of bravery: the unglamorous, costly kind—done in public, with real risk, when the moment demanded it.

Joseph of Arimathea was a respected member of the Jewish Ruling Council (Sanhedrin), a good and righteous man, a wealthy man, and—most revealingly—a disciple of Jesus, though privately/secretly. After the crucifixion, Joseph goes to Pilate and asks for Jesus’ body, then places Him in his own new tomb. That act wasn’t ceremonial—it was potentially reputation-ending and handling a dead body precluded him from participating in the Passover celebrations.

There is no verified first-century letter from Joseph of Arimathea that we can authenticate as historical. What does exist is a much later apocryphal narrative often called The Narrative of Joseph of Arimathea (sometimes treated like a “letter” because it’s written in Joseph’s voice). The Catholic Encyclopedia notes it as a medieval work, with early surviving manuscripts much later than the events.

So Joseph’s defining moment isn’t a sermon. It’s a burial.

Joseph’s moment matters because it combines three things we struggle to hold together:

1) Costly decency

Joseph steps forward when the risk is real. He attaches his name to a condemned man at the worst possible moment—after the crowd has moved on and the authorities are still watching.

2) “My tomb, not just my opinion”

He gives what’s truly his—his tomb, his resources, his security—rather than offering a safe, symbolic gesture.

3) Leaving secret discipleship behind

John’s description that Joseph was a disciple “secretly” lands like a mirror. Many of us prefer a faith that stays private because private faith rarely costs anything. Joseph shows what happens when belief becomes visible.

Closing question

Everyone has a worldview—a personal theology—even if they refuse the label.

So here’s the audit question Joseph forces on us:

What does your worldview cost you when it becomes inconvenient? And if you claim to follow Jesus: are you still a secret disciple… or do you show up when it’s finally time to show up?

![]()

Stuck at the helm? Let’s chart the next move.

If your business is wrestling with growth, team, or cash-flow puzzles—or you’re weighing how to fund the next big step—bring me your mess. I’ll bring a map.

Two simple, no-pressure ways to start:

-

Free Coaching Consultation

A focused 20–30 minutes to assess what’s blocking momentum and sketch 2–3 practical plays you can run this month. -

Free Capital Options Call

If you need financing for a new purchase, a refi, or a life event, we’ll review current options and model what’s smart—not just what’s available.

No jargon. No hard sell. Just clear ideas from someone who’s been in the wheelhouse when the water wasn’t calm.

Ready?

Chart a Coaching Call —or— Explore Capital Options +18582297199

Prefer email? Send a quick note to [jdevilliers@c2financial.com] with “Let’s talk” in the subject, and tell me what you’re navigating.

General Disclosure

This publication is for informational and educational purposes only and reflects the personal opinions of the author as of the date of publication. The views expressed do not necessarily reflect the views of any employer, client, or affiliated organization. The author is not selling, brokering, or offering any securities, investments, insurance, or other financial products through this publication.

No Professional Advice. Nothing herein is legal, tax, investment, accounting, or other professional advice. You should consult your own qualified advisors before making any decision.

No Recommendation or Solicitation. References to companies, markets, instruments, or strategies are illustrative and not recommendations, offers, or solicitations to buy or sell any product or service.

Sources and Accuracy. Some content summarizes or links to third-party sources believed to be reliable; however, the author does not warrant the completeness, timeliness, or accuracy of any information and assumes no responsibility for errors or omissions. Markets and laws change—information may become outdated without notice.

No Duty to Update. The author has no obligation to update any content, even if subsequent events make statements inaccurate.

Performance and Risk. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

No Client Relationship. Reading or interacting with this publication does not create a client, advisory, or fiduciary relationship with the author or [Your Company Name].

Third-Party Links. Links are provided for convenience and do not constitute endorsements. The author is not responsible for third-party content or policies.

Conflicts & Affiliations. The author may hold positions or have business relationships relevant to topics discussed and will endeavor to disclose material conflicts where appropriate.

© 2025 Johann de Villiers. All rights reserved. Contact: jdevilliers@C2Financial.com .

This licensee is performing acts for which a real estate license is required. C2 Financial Corporation NMLS #135622 is licensed by the California Department of Real Estate, Broker # 01821025; Arizona Department of Financial Institutions, Broker # 919209; Colorado Division of Real Estate; Florida Office of Financial Regulations, MBR3519 / MLD2635; Tennessee Department of Financial Institutions, DFI# 135622; Washington Mortgage Broker License MB-135622. Loan approval is not guaranteed and is subject to lender review of information. All loan approvals are conditional, and all conditions must be met by borrower. Loan is only approved when lender has issued approval in writing and is subject to the Lender conditions. Specified rates may not be available for all borrowers. Rate subject to change with market conditions. C2 Financial Corporation is an Equal Opportunity Mortgage Broker/Lender. The services referred to herein are not available to persons located outside the state of CA, AZ, CO, FL, TN and WA.

Johann de Villiers NMLS # 71252, CA DRE # 01746466, AZ #1040617, CO # 100534343,

FL #LO111486, TN # 71252, WA # MLO-71252

Related Posts